Every breakthrough and progress

It is our continuous pursuit of technological innovation

Every breakthrough and progress

It is our continuous pursuit of technological innovation

What development landscape awaits the epoxy resin and hardener industry in 2026? Based on the latest data from multiple market research institutions, we examine the core industry highlights from four dimensions: market size, demand structure, regional landscape, and product trends.

According to forecasts from various research institutions, the global epoxy hardener market will maintain steady expansion in 2026.

Global Market:

Fortune Business Insights projects continued growth in the global epoxy hardener market for 2026

QY Research data shows the global epoxy hardener market was valued at $3.726 billion in 2025, with expectations to reach $5.049 billion by 2032, representing a CAGR of 4.5% from 2026-2032

Business Research Insights estimates the global epoxy resin hardener market at approximately $4.83 billion in 2026, projected to reach $7.25 billion by 2035, with a ten-year CAGR of 4.3%

Global Growth Insights reports the 2025 global market size at $4.25 billion, expected to increase to $4.44 billion in 2026, up approximately 4.4% year-on-year

Chinese Market:

As the world's largest producer and consumer of epoxy resin, China's performance is particularly critical. Multiple institutions show the Asia-Pacific region accounting for 45%-55% of the global market, with China as the core growth engine. Rapid industrialization, infrastructure construction, and automotive industry development continue to drive demand for epoxy resins and hardeners.

Summary: Comprehensive data suggests the global epoxy hardener market will range between $4.4 billion and $4.8 billion in 2026, maintaining a steady growth rate of 4%-5%. Benefiting from manufacturing upgrades and emerging applications, the Chinese market is expected to grow faster than the global average.

Epoxy hardeners serve diverse downstream applications. In 2026, the following four areas will remain primary growth drivers:

Coatings represent the largest application area for epoxy hardeners, accounting for 34%-40% of the global market. Demand continues to grow for industrial anti-corrosion coatings, marine coatings, and floor coatings, particularly in infrastructure construction and maintenance, where high-performance, long-life epoxy coatings are increasingly sought.

The construction sector accounts for approximately 15% of the epoxy hardener market. Epoxy materials are preferred in concrete bonding, flooring systems, and protective coatings due to their excellent adhesion and durability. Urbanization and renovation projects provide sustained momentum for this segment.

The electrical and electronics sector accounts for about 10% of the global market. With 5G infrastructure expansion, electric vehicle adoption, and consumer electronics iteration, demand for electronic encapsulation and insulating materials continues to grow. This field requires hardeners with high purity, heat resistance, and electrical insulation properties—a high-value segment of the market.

The composites sector (including wind turbine blades) is the fastest-growing application. Global Growth Insights predicts high-performance composite applications will grow by over 45% during the forecast period. The trend toward larger wind turbine blades imposes higher requirements on the processing performance of infusion resins, presenting new challenges for hardener product upgrades.

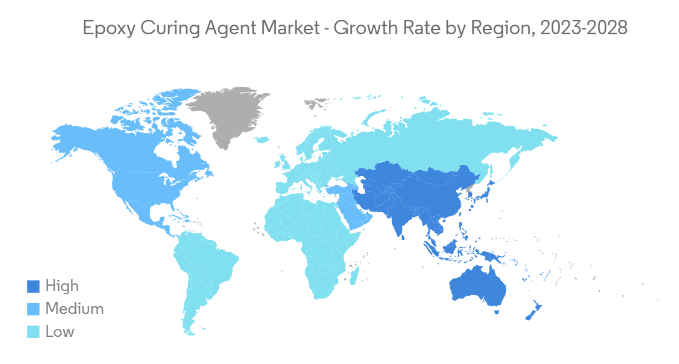

Asia-Pacific (especially China) continues to dominate the global market, accounting for 45%-55% of global demand. This stems from both manufacturing capacity concentration and sustained investment in infrastructure and new energy.

North America holds approximately 25%-30% of the global share, maintaining technological leadership in high-value segments such as aerospace composites and electronic encapsulation. Recent manufacturing reshoring policies and new energy project investments are injecting momentum into the regional market.

Europe accounts for about 20%, leading globally in demand for bio-based and low-VOC hardeners driven by environmental regulations. Wind blade manufacturing and automotive lightweighting are also key growth points in the European market.

In 2026, epoxy hardener product upgrades show three clear directions:

Increasingly strict VOC regulations are driving the industry toward solvent-free, high-solid, and waterborne systems. More significantly, downstream customer recognition of green products is growing—environmentally friendly formulations (including bio-based and low-VOC hardeners) now account for nearly 10% of the total market.

Bio-based hardeners are no longer conceptual products. Bio-based epoxy hardeners launched by international giants like BASF and Mitsubishi Chemical between 2023-2025 accounted for 12% of globally newly introduced sustainable products. As upstream bio-based raw material capacity expands, bio-based hardener costs are approaching traditional products, with market acceptance gradually increasing.

Wind Power Sector: Balancing longer infusion windows with faster demolding times imposes higher requirements on hardener reactivity control

Electronics Sector: Miniaturization trends demand curing systems with higher heat resistance (high Tg) and lower ionic impurity content

Low-Temperature Curing: Demand increases for products capable of proper curing at 5-10°C for winter construction, emergency repairs, and similar scenarios

Single hardener types increasingly struggle to meet complex application requirements. Blending different hardener structures (aliphatic amines, cycloaliphatic amines, polyamides, etc.) to achieve tailored performance is becoming mainstream. This "formulation service" capability is emerging as a core competitiveness indicator for hardener manufacturers.

Industry progress faces challenges. In 2026, epoxy hardener companies must address:

Raw Material Price Volatility: Prices of key raw materials (amines, anhydrides) fluctuate frequently due to global supply chain and geopolitical factors, challenging cost control and pricing strategies

Rising Environmental Compliance Costs: Increasingly stringent regulations on chemical production and use require continuous investment to maintain compliance

Health and Safety Concerns: Certain epoxy hardeners pose health risks during production and use (skin irritation, respiratory sensitivity), driving the industry toward less toxic, less irritating formulations

The 2026 epoxy resin and hardener industry presents a pattern of "steady overall growth with continuous structural optimization." The market no longer simply asks "can it cure?" but rather "what value does it provide after curing?" For industry participants, rather than chasing every trend, focusing on respective advantageous areas and finding suitable paths in environmental orientation, high performance, and specialization may prove more valuable.

As industry members, we will continue monitoring market dynamics, optimizing product performance, and working with upstream and downstream partners to promote healthy industry development.

Highfar National Service Hotline